EPISODE · May 6, 2026 · 10 MIN

Fundamentals of Investing — Episode 3 — Assets and Liabilities

from The Unlearned Investor Podcast · host The Unlearned Investor

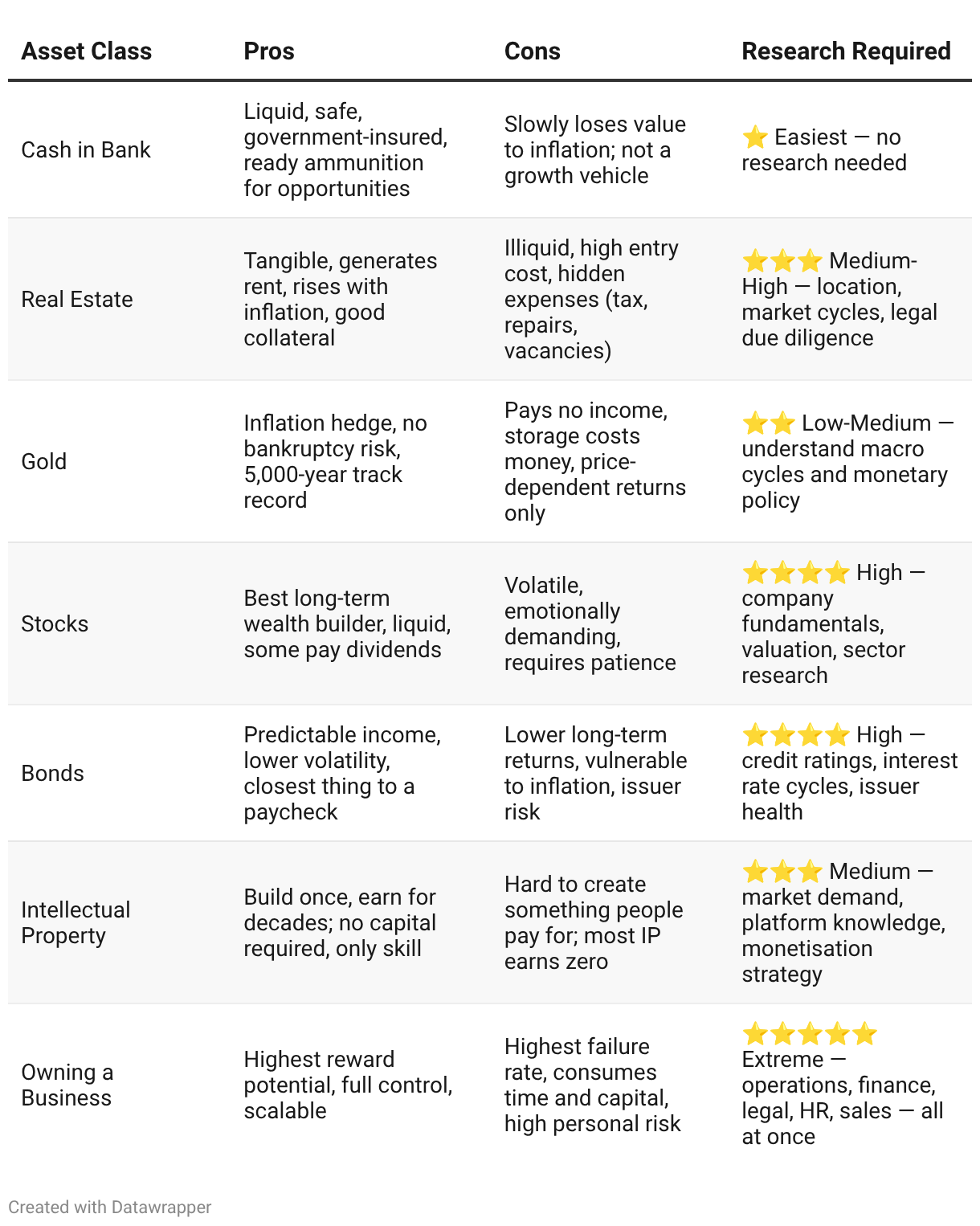

In Episode 2, we saw how Central Banks quietly chip away at the value of your cash. Inflation is the slow leak in the boat.So the obvious next question is — if cash is melting, where do I actually put my money?That’s where Assets come in. But before we talk about what to buy, we have to settle a much bigger argument — one that confuses 90% of people.What is an asset, really?Ask your neighbor, and they’ll point at their new SUV. Ask an accountant, and they’ll laugh.1. The Simple Test: Does It Feed You, or Eat You?Forget textbooks for a second. Here’s the cleanest definition you’ll ever hear.An Asset puts money in your pocket. A Liability takes money out.That’s it. That’s the whole game.Your rental property collects rent every month — it feeds you. Your fancy car loses value the moment you drive it off the lot, then demands fuel, insurance, and repairs forever — it eats you.Same person. Same garage. One is feeding them, one is eating them.2. The Seven Asset BucketsSo what actually qualifies as an asset for a regular person trying to build wealth? Seven buckets to know — each with its own rhythm, its own reward, and its own catch.3. Wait — Is My Job an Asset?Here’s the question that makes most people pause.“My job pays me every month. Doesn’t that make it an asset?”It’s a fair question. And the honest answer is — no.You don’t own your job. Your job owns you.It can be taken away by a layoff, a recession, a health scare, or simply by getting older. You’re not the owner of the arrangement — you’re the rental property. The company is renting your time, and they can end the lease whenever they choose.Your job is the engine that buys assets. But the engine itself isn’t the asset.That’s the entire point of investing — to build a portfolio so strong that one day, the engine becomes optional.4. The Liability in DisguiseHere’s where most people get tricked.A car is not an asset. It loses roughly 20% of its value the day you drive it off the lot. Your phone is not an asset. Your designer watch is not an asset. Your credit card is the opposite of an asset — it’s a tool that lets liabilities multiply faster than your salary ever can.We’ll call this The Lifestyle Trap. The slow drift where every pay rise brings a bigger car, a bigger phone, a fancier holiday — and somehow the bank balance never actually moves.The trap isn’t the items themselves. The trap is mistaking them for wealth.5. Are All Liabilities Bad?No. And this is where most people get it wrong.Not all liabilities are created equal. There’s a sharp line between Destructive Liabilities and Strategic Liabilities — and confusing the two is one of the most expensive mistakes a regular investor makes.A Destructive Liability drains your money and gives you nothing productive in return. A car loan on a vehicle that sits in your driveway. Credit card debt charging 20% interest. A personal loan taken for a holiday. These are financial leaks — money leaving your pocket with no asset growing on the other side.A Strategic Liability, on the other hand, is debt you take on deliberately to acquire something that earns more than it costs. A mortgage taken on a rental property that pays rent above the loan installment — that’s a liability working for you. A business loan that funds equipment generating more profit than the interest — that’s a liability being used as a lever.Think of it this way. A lever — even a heavy one — helps you lift something bigger than you could alone. But a lever used carelessly crushes you.The questions to ask before taking on any debt are simple. Will this liability fund an asset? Will that asset earn more than the liability costs? And what happens to me if the income from that asset disappears tomorrow?If the answers are yes, yes, and “I survive” — it may be a strategic liability worth considering.If the answers lead back to — “I just want it” — that’s a destructive liability dressed up in good intentions.The goal is never zero debt. The goal is zero wasteful debt.6. The Gray ZoneSome things are both — and that’s fine to admit.Your home is the classic example. It’s not a pure asset — it eats you with mortgage interest, property tax, maintenance, and insurance. But it’s not a pure liability either — it shelters you, it tends to rise with inflation, and someday you’ll own it free and clear.A car used for a delivery business? Asset. The same car for weekend joyrides? Liability.The point isn’t to memorize a list. The point is to ask one question every time money leaves your wallet — is this going to feed me, or eat me?THE BOTTOM LINEThe goal of an individual investor saving for retirement is simple to say and hard to do — invest in assets, reduce liabilities, and build a portfolio that takes care of you when you can no longer take care of yourself.Trust me on this — that day comes sooner than you think.Three rules should guide every decision you make.Rule 1 — Never lose your capital. Capital is the seed. You can grow more from a small seed, but you can grow nothing from nothing. Protecting what you already have always comes before chasing what you don’t.Rule 2 — You only have to beat inflation. You’re not a fund manager. You don’t have a quarterly review. You’re not racing Wall Street, your neighbor, or the guy bragging about crypto at dinner. The only benchmark that matters is the rising cost of bread.Rule 3 — Diversify by purpose, not just by name. Some of your assets should pay you regular income — that’s what bonds, dividend stocks, and rental property are for. Others should grow quietly in the background — that’s what growth stocks, gold, and businesses are for. A real portfolio has both.A successful retirement isn’t a magic number. It isn’t ten times your salary or fifteen times your expenses or whatever the latest financial article declares.It’s much simpler than that.Write down your monthly expenses today. Multiply by inflation over however many years you have left. That’s roughly the number your investments need to cover when your paycheck stops. Any portfolio that reaches that number — without risking your capital — is, by definition, a great investment for you.That last word matters. For you. Not for anyone else. Not for the market. Not for your brother-in-law’s stock tips.Your retirement. Your number. Your pace.DISCLAIMER: I am not a financial advisor. This is for educational purposes only. Always do your own research and speak with a certified financial professional before making investment decisions.Now that we know what real assets look like and how to think about debt, the next question is — how do retail investors actually buy these assets? In Episode 4, we’ll walk through the different investment products available to build your wealth over time and plan confidently for retirement.Thanks for reading! This post is public so feel free to share it.This Substack is reader-supported. To receive new posts and support my work, consider becoming a free or paid subscriber. Get full access to The Unlearned Investor at unlearnedinvestor.substack.com/subscribe

NOW PLAYING

Fundamentals of Investing — Episode 3 — Assets and Liabilities

No transcript for this episode yet

Similar Episodes

Mar 26, 2026 ·1m

Mar 19, 2026 ·34m

Feb 18, 2026 ·11m

Feb 11, 2026 ·45m