EPISODE · Mar 12, 2026 · 7 MIN

The College Debt Crisis is Fake

from The College Question Podcast · host Dan Currell

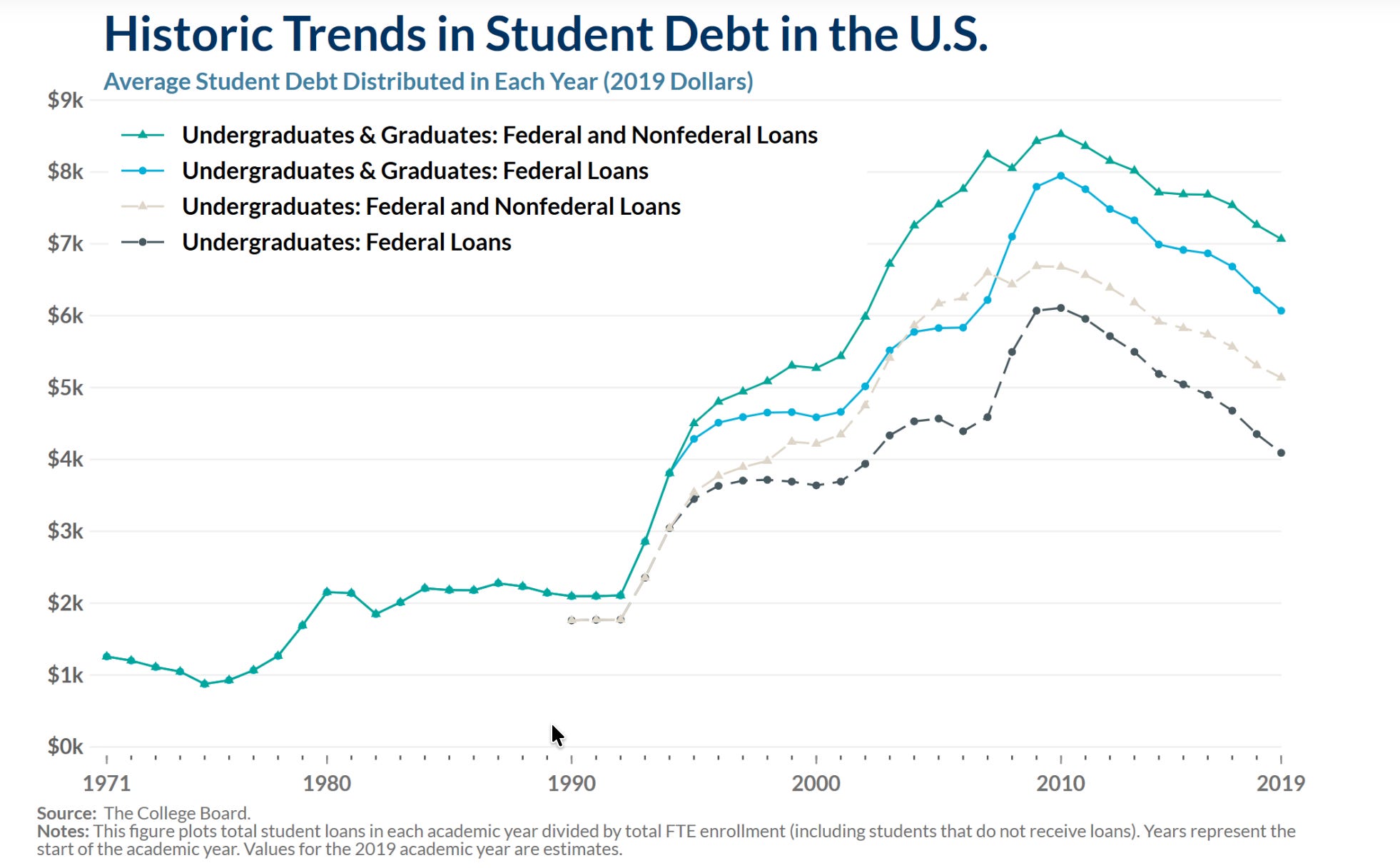

Today we continue TCQ’s series on Ten Things We Get Wrong About College with …#6: There’s a college debt crisis!(No. But there are problems.)Conventional wisdom is that college costs a fortune because students can just borrow the money to pay for it, leading to higher prices, and that’s why we have a college debt crisis.This is appealing logic, but it’s wrong as far as college goes because undergraduates aren’t allowed to borrow very much. It does describe graduate school, where until recently there were no borrowing limits. As I laid out in article #9 in this series, the cost of college stopped rising a decade or more ago, partly because the money supply was pretty limited.The Very Short VersionAn undergraduate student can borrow $31,000 from the federal government for college. Not for a year of college - for all of college. Because people don’t seem to know this, it’s pretty common for families to be shocked when they learn that their child can’t borrow the full cost of college. The loan limits are detailed in the Federal Student Aid Handbook.Source: https://youngamericans.berkeley.edu/2021/12/historic-trends-in-us-student-debt/The Somewhat Longer VersionOver a standard ten-year repayment period, $31,000 in federal loans works out to a monthly payment of roughly $280 to $310, depending on the interest rate. Most students borrow less than the maximum, and the amount students borrow has been declining in recent years. The average undergraduate leaves college with about $25,000 to $29,000 in federal debt — again, for the whole degree.This is why graduates of completely different schools have pretty much the same monthly loan payment. Northeastern: $257. University of Arkansas: $228. Lipscomb University: $207. That is not the crushing debt that got us into a national conversation about student debt relief.Of course, federal loans aren’t the only way to borrow for college. There are three other channels.Parent loans. Until recently, federal Parent PLUS loans had no borrowing limit, and some families would get themselves $200,000 in debt for an undergraduate degree. As of this year, the law caps these loans at $20,000 per year and $65,000 total. So now, combined with student loans, a family can take out a maximum of $96,000 for an undergraduate degree.Private loans. Private student loans make up $140 billion, or 8% of the $1.8 trillion total student loan market. The other 92% is federal. Private loans are underwritten, so the lender will limit how much you can borrow based on creditworthiness.State loans. Some states have student loan programs – here are examples from Minnesota and Texas. They are small – in total, perhaps $1 billion a year.Where the Real Problems AreSo if the typical undergraduate leaves school with a $250 monthly loan payment, where’s the crisis? Three places:* Students who borrow and don’t finish. 60% of borrowers who default on their loans never completed a degree. This is a matching problem (getting people into the right field of study) and a completion problem, but it’s not a debt problem, since it would be better for them to have a $200 payment and the right degree than no payment and no degree.* Balances that grow. Interest rates are pegged to the 10-year Treasury note, so lately they have been high — 6.53% for undergraduates in 2024-25, and 7.94% for graduate students. When borrowers defer payments, enter forbearance, or make income-driven payments, their balances grow. This New York Times Opinion piece and infographic conveys this point very well.* Graduate school debt. 57% of all student debt is held by households with at least one graduate degree. There was no cap on federal borrowing for graduate students until this year, so a law or medical student could borrow $250,000 or more — and many did. Starting this year, borrowing is capped at $20,500 per year and $100,000 in aggregate for most graduate students, or $50,000 per year and $200,000 for professional programs like law and medicine.It’s worth noting that while doctors and lawyers with large debt balances get the headlines, they also tend to have the incomes to manage those payments. Truly academic Ph.D. programs tend to be funded, so students in those often graduate with little or no debt. But the troubling cases are graduate students in fields like education, social work, and the arts — where the degrees still cost a lot, but the jobs they lead to don’t command high salaries.In sum, there’s a student debt problem, and arguably even a crisis, but it isn’t a college debt problem. Parent borrowing was a problem in certain cases, and massive graduate borrowing was by far the biggest issue. New limits on Parent PLUS, graduate and professional school borrowing may make a difference, and some schools will likely have to adjust their pricing as a result.Tomorrow, we’ll continue Ten Things We Get Wrong About College with:#5 — Ugh! [Perfect Daughter] has to take the SAT. (What for? Let’s get into it.)Previous posts …* #10 - College is harder to get into than ever! (It’s never been easier.)* #9 - College is more expensive than ever! (Tuition has been flat for 15 years.)* #8 - Ugh. We have to fill out the FAFSA. (Maybe. Here’s what to know.)* #7 - Colleges are closing! (Yes, but none you’ve heard of.)To come …* #5 - Ugh! [Perfect Daughter] has to take the SAT. (What for? Let’s get into it.)* #4 - Well, I guess a sports scholarship is the ticket. (They’re mostly fake.)* #3 - I bet expensive schools spend a lot on the student experience. (Sometimes, if they feel like it. Here’s how to find out.)* #2 - Ivy League graduates make the big bucks. (Not usually - for pretty obvious reasons.)* #1 - [Handsome Prince] should go to college in [country], where it’s free! (It’s not, which is one of the reasons nobody does this.)Other recent posts …* Sunday Charticle: What Do Students Major In?* How colleges discovered the virtue of geographical diversity – and other shenanigans* Launching The College QuestionThe College Question is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber. This is a public episode. If you'd like to discuss this with other subscribers or get access to bonus episodes, visit thecollegequestion.substack.com/subscribe

NOW PLAYING

The College Debt Crisis is Fake

No transcript for this episode yet

Similar Episodes

Mar 26, 2026 ·1m

Mar 19, 2026 ·34m

Feb 18, 2026 ·11m

Feb 11, 2026 ·45m