PODCAST · business

Series 32 - The SAF-T Architecture X-Ray: What Your Data Looks Like to a Tax Authority

by Ryigit

SAF-T does not create data quality problems. It reveals them. The chart of accounts mismatches, the missing master data, the inconsistent transaction classifications, the intercompany positions that have never reconciled — these problems existed before the SAF-T obligation arrived. The obligation simply makes them visible to the tax authority in a structured format that leaves nowhere to hide. The SAF-T Architecture X-Ray examines what SAF-T actually exposes.Hosted by Rıdvan Yiğit | Founder & CEO, RTC Suitertcsuite.com · [email protected] · linkedin.com/in/yigitridvan

-

4

Series 32 - The Deep Dive: The SAF-T Financial Architecture X-Ray

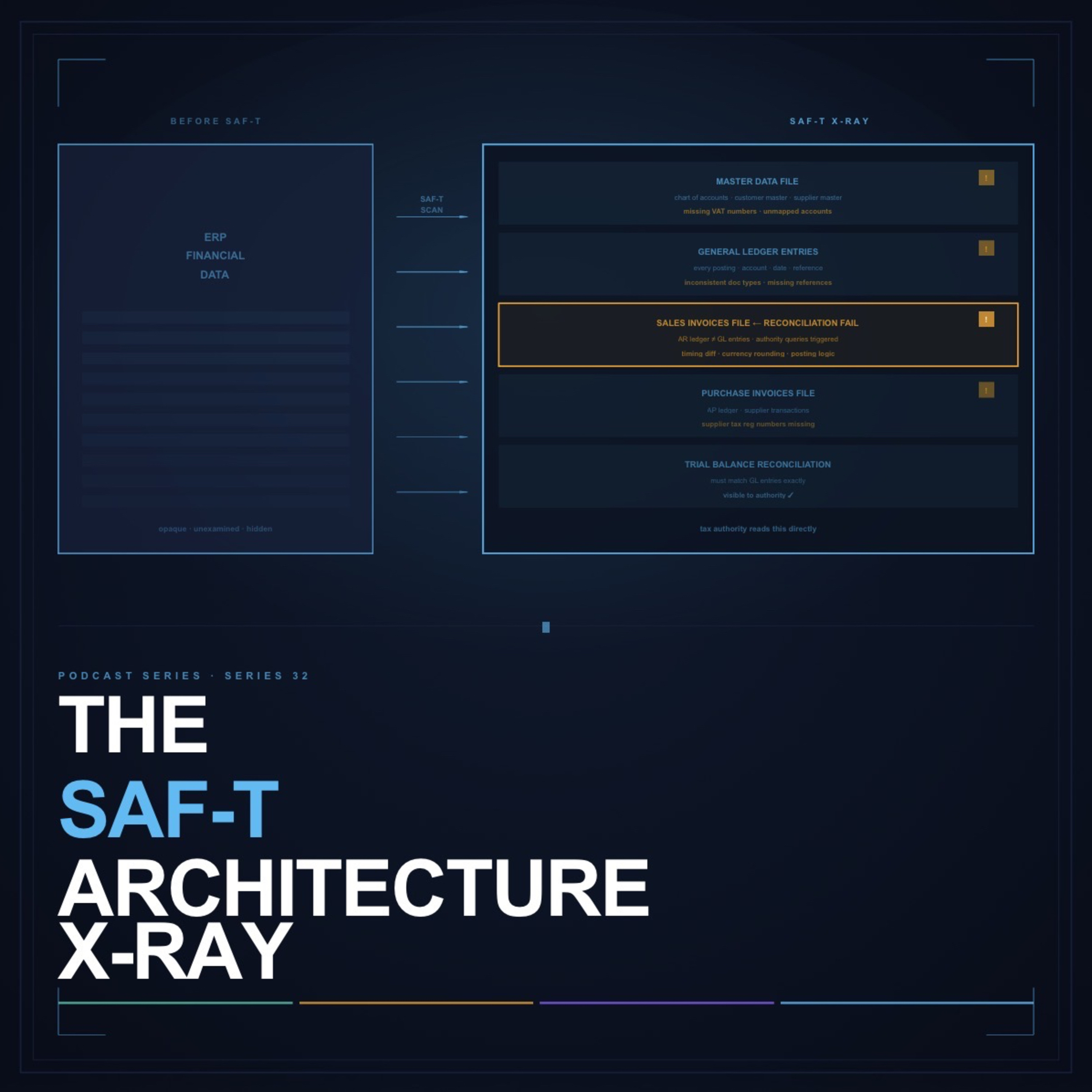

SAF-T is not a compliance exercise. It is the most comprehensive financial data architecture assessment most organisations will ever conduct — applied under regulatory deadline, with the results submitted directly to the tax authority. This deep dive builds the complete picture of what the SAF-T financial architecture X-ray reveals, what it requires to fix, and how the organisation that does the SAF-T implementation correctly emerges with a financial data foundation that is qualitatively better than the one it started with.We begin with the SAF-T schema anatomy — the four core files that every SAF-T implementation must produce and what each file reveals about the underlying data architecture. The master data file reveals the completeness and consistency of the organisation's chart of accounts, customer master, and supplier master. Every missing tax registration number, every account without a standard taxonomy mapping, every customer with an invalid VAT number appears here as a validation error that the authority's schema will reject. The general ledger entries file reveals the transaction-level completeness of the financial record: every posting must carry a valid account code, a valid document reference, a valid tax point date, and a valid entity identifier. The sales invoices file and purchase invoices file reveal whether the transactional data in the AR and AP ledgers is consistent with the general ledger entries — and inconsistencies between these files are the errors that trigger authority queries and audit attention.We then examine the remediation programme in full: the chart of accounts rationalisation that creates a clean mapping between the organisation's internal account structure and the SAF-T standard taxonomy; the master data governance programme that populates missing tax registration fields, validates existing VAT numbers against authority registries, and establishes the ongoing processes that prevent master data from degrading again; the transaction classification review that ensures document types, tax codes, and posting references are applied consistently across the ERP; and the reconciliation framework that verifies that the four SAF-T files are internally consistent before submission.We address the ongoing architecture: how the SAF-T submission is maintained as a continuous data quality monitoring tool rather than a periodic compliance exercise; how the master data governance framework prevents the regression of data quality between submissions; how the chart of accounts rationalisation is extended to support the other real-time reporting requirements that will follow SAF-T in the regulatory sequence; and how the CFO uses the SAF-T submission quality metrics as a leading indicator of the overall financial data architecture health. The organisation that treats SAF-T as an X-ray rather than a filing obligation uses it to build the data foundation that the next decade of finance transformation requires.Keywords: SAF-T financial architecture X-ray, SAF-T deep dive architecture, SAF-T schema anatomy, SAF-T master data file, SAF-T general ledger file, SAF-T data architecture complete, SAF-T remediation programme, SAF-T chart of accounts rationalisation, SAF-T master data governance, SAF-T transaction classification, SAF-T reconciliation framework, SAF-T financial data foundation, SAF-T architecture deep dive, SAF-T data quality monitoring, SAF-T ERP architecture complete, SAF-T financial data architecture design, SAF-T submission quality, SAF-T data governance ongoing, SAF-T architecture X-ray complete, SAF-T finance transformationAbout the HostRıdvan Yiğit is the Founder & CEO of RTC Suite — the world's first Autonomous Compliance and Payment Intelligence platform, built natively on SAP BTP and operating across 80+ countries.Connect with Rıdvan:🔗 linkedin.com/in/yigitridvan✉ [email protected]📞 +90 545 319 93 44Learn more about RTC Suite:🌐 rtcsuite.com

-

3

Series 32 - The Debate: Should SAF-T Force an ERP Data Overhaul?

The debate that SAF-T implementations consistently trigger is not about compliance. It is about scope. Every organisation implementing SAF-T faces the same decision point: when the data quality work required to produce a valid SAF-T file reveals architectural problems in the ERP data model, does the organisation fix the symptoms — patch the data, produce the file, move on — or fix the cause — redesign the data architecture that produced the problems, and use the SAF-T mandate as the business case for the ERP data overhaul that the finance function has needed for years?The case for treating SAF-T as a mandate for an ERP data overhaul argues from the cost of the alternative. Patching data for SAF-T compliance without fixing the underlying architecture produces a SAF-T file that passes validation but does not reflect a well-structured financial data model. The next SAF-T submission requires the same patches. The audit that follows the SAF-T submission may identify discrepancies between the SAF-T data and the underlying ERP data that the patches created. And every other compliance initiative that depends on the same data — CTC, real-time reporting, continuous close — inherits the same architectural problems. The SAF-T mandate is the best business case the finance function will get for the ERP data overhaul, because it comes with a regulatory deadline, a clear quality standard, and a direct consequence of non-compliance.The case against architectural overhaul argues from delivery risk. An ERP data overhaul in the context of a compliance deadline is the highest-risk configuration of any IT project: the deadline is fixed, the scope is uncertain, the stakeholder alignment is difficult, and the failure mode — a SAF-T submission that fails validation because the overhaul was not completed in time — is public and regulatory. The organisations that have successfully delivered SAF-T on time have generally done so by scoping the compliance work tightly, fixing the minimum required to produce a valid file, and treating the architectural improvement as a follow-on programme rather than a prerequisite.Keywords: SAF-T ERP overhaul debate, SAF-T forces ERP overhaul, SAF-T data architecture overhaul, SAF-T ERP data debate, should SAF-T ERP overhaul, SAF-T data overhaul decision, SAF-T ERP data architecture, SAF-T overhaul debate, SAF-T ERP architecture decision, SAF-T compliance vs overhaul, SAF-T data architecture decision, SAF-T ERP overhaul risk, SAF-T overhaul business case, SAF-T architecture overhaul, SAF-T ERP overhaul complianceAbout the HostRıdvan Yiğit is the Founder & CEO of RTC Suite — the world's first Autonomous Compliance and Payment Intelligence platform, built natively on SAP BTP and operating across 80+ countries.Connect with Rıdvan:🔗 linkedin.com/in/yigitridvan✉ [email protected]📞 +90 545 319 93 44Learn more about RTC Suite:🌐 rtcsuite.com

-

2

Series 32 - The Critique: SAF-T Exposes Broken Data Architecture

SAF-T is the most effective data architecture audit tool that most finance functions have ever been subjected to — not because it was designed as an audit tool, but because it requires the organisation to produce a structured, complete, internally consistent representation of its financial data that the tax authority can examine at transaction level. This requirement, applied to ERP systems that were not designed for this level of structured output, reveals architectural failures that have been invisible to finance teams for years.The failures that SAF-T exposes fall into three categories. The first is mapping failures: the organisation's chart of accounts does not map cleanly to the SAF-T standard account taxonomy because the chart of accounts was built for management reporting purposes and contains accounts that have no standard tax equivalent, accounts that combine multiple tax treatments, and accounts that have been used inconsistently across entities. Producing a valid SAF-T mapping requires resolving every ambiguity in the chart of accounts — which means making accounting policy decisions that were deferred when the chart was built.The second is completeness failures: the SAF-T schema requires fields that the ERP does not consistently populate. Supplier tax registration numbers that were never entered. Customer VAT numbers that were entered in free-text format rather than validated format. Document reference numbers that were populated manually and inconsistently. Transaction dates that do not match the tax point dates because the posting process did not enforce the distinction. Each of these gaps must be remediated before the SAF-T file can be produced without errors.The third is consistency failures: the same underlying transaction is represented differently in different parts of the ERP. The sales invoice that generated the output tax appears in the VAT ledger, the accounts receivable ledger, and the general ledger — but the amounts do not reconcile because of timing differences, currency rounding, or posting logic that was not designed for cross-ledger consistency. SAF-T requires consistency. The ERP was not designed to enforce it.Keywords: SAF-T exposes data architecture, SAF-T broken data architecture, SAF-T data architecture failure, SAF-T exposes ERP problems, SAF-T chart of accounts, SAF-T data architecture critique, SAF-T ERP architecture, SAF-T exposes finance data, SAF-T data consistency, SAF-T mapping failure, SAF-T completeness failure, SAF-T ERP data quality, SAF-T architecture exposure, SAF-T financial data architecture, SAF-T data architecture problemsAbout the HostRıdvan Yiğit is the Founder & CEO of RTC Suite — the world's first Autonomous Compliance and Payment Intelligence platform, built natively on SAP BTP and operating across 80+ countries.Connect with Rıdvan:🔗 linkedin.com/in/yigitridvan✉ [email protected]📞 +90 545 319 93 44Learn more about RTC Suite:🌐 rtcsuite.com

-

1

The Brief: SAF-T Forces a Massive Data Cleanup

SAF-T mandates do not arrive in a vacuum. They arrive in organisations that have been accumulating data quality debt for years — in ERP systems that were configured for operational efficiency rather than tax reporting accuracy, in chart of accounts structures that were designed for management reporting rather than statutory compliance, in master data records that were created quickly and never reviewed. SAF-T makes this debt visible, immediately, in a format that the tax authority can query directly.The data cleanup that SAF-T forces is not the cleanup organisations would have chosen to prioritise. It is the cleanup that SAF-T's schema makes mandatory: every transaction must have a valid general ledger account code mapped to the standard SAF-T taxonomy. Every customer and supplier record must have a complete tax registration number. Every document must have a consistent document type classification that maps to the SAF-T document types. Every balance must reconcile between the SAF-T general ledger file and the SAF-T trial balance file. None of these requirements are new in principle — they are basic standards for financial data quality that organisations should have been maintaining all along. SAF-T simply enforces them with a deadline and a direct submission to the authority.The brief this episode makes is practical: the SAF-T data cleanup is not a compliance overhead. It is the most valuable data quality investment most organisations will make in the next five years — because the data that SAF-T cleans is the same data that real-time analytics requires, that continuous close depends on, and that AI-driven finance tools need to produce reliable outputs. The organisation that does the SAF-T cleanup properly is not just getting compliant. It is building the data foundation that every other finance transformation initiative in the roadmap depends on.Keywords: SAF-T data cleanup, SAF-T data quality, SAF-T forces data cleanup, SAF-T ERP data, SAF-T data architecture, SAF-T master data, SAF-T chart of accounts, SAF-T compliance data, SAF-T data quality ERP, SAF-T data cleanup finance, SAF-T financial data, SAF-T data preparation, SAF-T ERP cleanup, SAF-T data quality mandate, SAF-T compliance cleanupAbout the HostRıdvan Yiğit is the Founder & CEO of RTC Suite — the world's first Autonomous Compliance and Payment Intelligence platform, built natively on SAP BTP and operating across 80+ countries.Connect with Rıdvan:🔗 linkedin.com/in/yigitridvan✉ [email protected]📞 +90 545 319 93 44Learn more about RTC Suite:🌐 rtcsuite.com

No matches for "" in this podcast's transcripts.

No topics indexed yet for this podcast.

Loading reviews...

ABOUT THIS SHOW

SAF-T does not create data quality problems. It reveals them. The chart of accounts mismatches, the missing master data, the inconsistent transaction classifications, the intercompany positions that have never reconciled — these problems existed before the SAF-T obligation arrived. The obligation simply makes them visible to the tax authority in a structured format that leaves nowhere to hide. The SAF-T Architecture X-Ray examines what SAF-T actually exposes.Hosted by Rıdvan Yiğit | Founder & CEO, RTC Suitertcsuite.com · [email protected] · linkedin.com/in/yigitridvan

HOSTED BY

Ryigit

CATEGORIES

Loading similar podcasts...

URL copied to clipboard!