EPISODE · Feb 8, 2026 · 22 MIN

**Sunday Recap & Portfolio Discussion

from GoldFix · host VBL

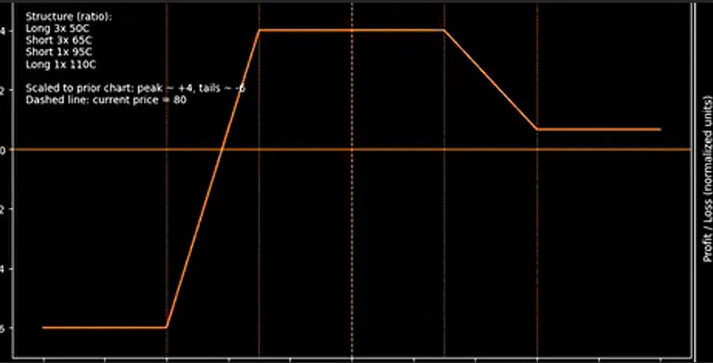

This is a free preview of a paid episode. To hear more, visit vblgoldfix.substack.comHousekeeping: Hartnett plus some extras will be out at noon today. Have a good oneI. Market Recap and Structural Context (approx. 00:03–00:21)A. Friday’s Price Action and Volatility Shock* Description of the “jaw-dropping” move and why it stands out historically* Comparison to prior market dislocations (1990s scandals, 2008–2011, Brexit, etc.)* Emphasis on unprecedented speed and range compression/expansion in metalsB. Open Interest Collapse as the Core Signal* Short-term vs multi-year COMEX open interest charts* Open interest at cycle lows and all-time lows despite higher prices* Interpretation: exchange relevance erosion rather than bearish positioning* Conceptual shift of liquidity and speculation from COMEX to ShanghaiC. Market Mechanics Driving the Move* Short covering on rallies and on selloffs* Banks prioritizing contract recovery over price sensitivity* Explanation of why violent reversals are occurring intraday rather than over weeksD. Technical Framing* Fishhook formation and long-wick reversals* Bear flag risk versus breakout invalidation levels* Gold vs silver divergence (gold structurally stronger, silver lagging but stabilizing)* Key support “ledges” and behavioral confirmation from large playersII. Condor Strategy Explanation (approx. 00:22–00:32)A. Why Options Matter Here* Volatility regime change makes naked options unreliable* Core principle: everything must be spread* Options framed as volatility instruments rather than directional betsB. Condor Structure (Beginner Level)* Definition of a standard call condor* Breakdown of legs and payoff symmetry* Explanation of max gain vs max loss* Market assumption: range-bound settlementC. Alternative Interpretations (Intermediate Level)* Condor viewed as:* Long call spread + short call spread* Short strangle with defined risk* Synthetic combinations of puts and calls* Key rule: properly hedged calls and puts are functionally equivalentD. Probability and Expected Value Logic* Risk/reward trade-off explained via expected value* Why a “bad” risk/reward can still be a good trade* Importance of width expansion during high volatility regimesIII. Personal Portfolio Risk Position and Ratio Condor (approx. 00:32–end)A. Transition from Neutral to Directional Bias* Why pure neutrality is rejected* Expressed belief: if wrong, market is more likely wrong to the upsideB. Ratio Condor Construction* Modification of the standard condor to skew bullish* Increasing exposure on the lower strike side* Reducing or eliminating upside loss* Resulting asymmetry:* Larger downside risk* No upside loss if market ralliesC. Risk Trade-Offs and Intentional Asymmetry* Acceptance of increased downside loss in exchange for upside immunity* Position framed as neutral-to-bullish volatility harvest, not a price bet* Emphasis on delta management rather than fixed strikesD. Position Management Philosophy* Partial deployment (two-thirds on, one-third remaining)* Strikes adjusted dynamically with price movement* Core principle: married to structure and deltas, not strikes

NOW PLAYING

**Sunday Recap & Portfolio Discussion

No transcript for this episode yet

Similar Episodes

No similar episodes found.

Similar Podcasts

No similar podcasts found.