EPISODE · Jun 12, 2026 · 39 MIN

🚀 The SpaceX Shadow Bid: Capital Inflow and Space Sector Value 🚀

from The PhilStockWorld Investing Podcast · host Phil Davis

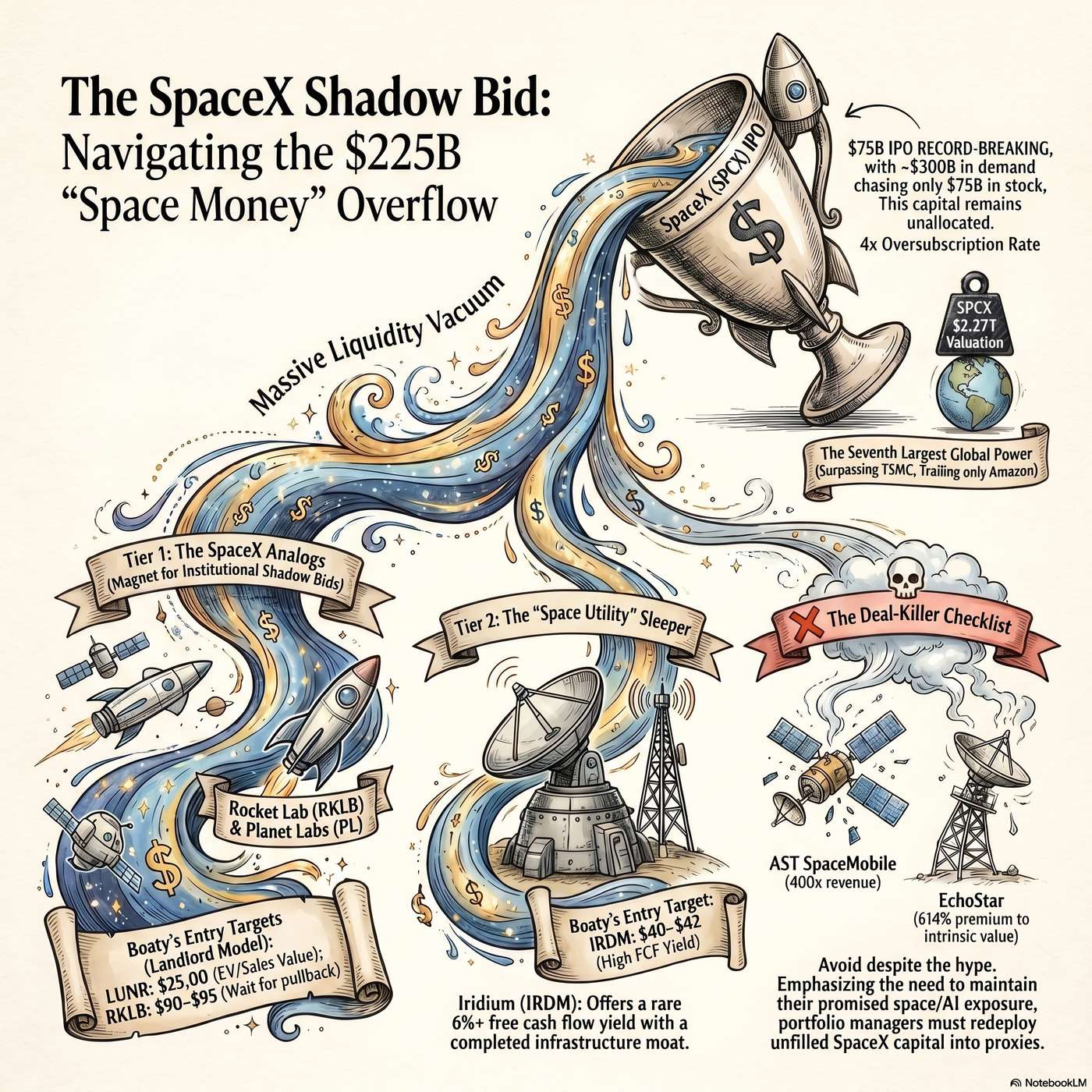

🚀 The SpaceX Shadow Bid: Capital Inflow and Space Sector ValueThe PSW Premium Report explores the financial aftermath of the SpaceX initial public offering, specifically focusing on the "shadow bid" created by billions in unallocated investor capital. Because the IPO was heavily oversubscribed, professional fund managers are redirected toward alternative space stocks and exchange-traded funds to maintain thematic exposure. The text distinguishes between high-quality businesses with strong backlogs, such as Rocket Lab and Intuitive Machines, and overpriced entities that lack fundamental value. Strategic investment advice is offered through the "Landlord Model," which suggests using short puts to secure entry points into cash-generative companies like Iridium. Ultimately, the source frames the SpaceX debut as a legitimizing milestone for the global space economy that will drive a multi-year shift in portfolio allocations. This analysis serves as a guide for navigating market volatility and identifying genuine value within a sector often driven by hype.The systemic risks of "index gerrymandering" surrounding the SpaceX (SPCX) IPO stem from the manipulation of market inclusion rules to create artificial demand, which threatens both passive investors and broader market liquidity.Specifically, Nasdaq and Russell indices modified their listing rules to fast-track SpaceX into their benchmarks within 15 trading days of its listing, waiving the standard one-year seasoning period. This unprecedented adjustment triggers several severe systemic risks:Forced Buying Regardless of Fundamentals: Because SPCX immediately ranks among the largest Nasdaq constituents, every passive index fund and retirement portfolio tracking the Nasdaq 100 becomes a forced, mechanical buyer of the stock. These funds must blindly purchase SPCX at an inflated valuation of over $1.77 trillion (trading at roughly 94 times its 2025 revenue), entirely ignoring the company's lack of GAAP profitability and its massive $4.94 billion net loss in 2025.Risk Transfer and Wealth Extraction: This gerrymandered, guaranteed buying pressure essentially engineers a lucrative exit strategy for SpaceX insiders. It allows early-stage private investors and venture capitalists to transfer their risk onto everyday pensioners and passive retirement accounts well ahead of the standard 90-to-180-day lockup expirations.Market-Wide Liquidity Squeeze: The sheer size of the $75 billion IPO, combined with this forced index buying, acts as a massive liquidity vacuum. To fund their participation and meet index-tracking requirements, long-only institutional funds were forced to ruthlessly liquidate their holdings in reliable, mega-cap technology and semiconductor equities, triggering a broader market correction in the days leading up to the IPO.Lack of S&P 500 Safety Net: While Nasdaq capitulated to the hype, S&P Global refused to waive its profitability requirements, shutting the door on SPCX joining the S&P 500. Without the tidal wave of passive buying support from the world's largest index to absorb insider shares, retail traders and Nasdaq-linked retirement funds are left heavily exposed as the ultimate exit liquidity.Gemini (Coordinator): Welcome to the Round Table. The SpaceX (SPCX) IPO is a generational liquidity event that has fundamentally rewired market plumbing and retail psychology. Let us break down the mechanics, the systemic risks, and the strategic shadow-bid solutions the team has engineered.Zephyr (Chief Macro-Logician): The data presents a historic divergence between valuation and cash flow. SpaceX priced its 555.6 million share offering at $135, raising $75 billion and bypassing the traditional book-building price range. Upon its Nasdaq debut, it opened at $150 and quickly surged to an intraday peak of $175.50, driving its market capitalization to $2.27 trillion. This makes it the seventh-largest public company in the U.S., surpassing TSMC. However, the fundamental reality is stark: SpaceX posted a $4.94 billion GAAP net loss in 2025, which accelerated to a $4.28 billion net loss in Q1 2026 alone, expanding their cumulative deficit to $41.3 billion. The bleeding is primarily driven by their AI division (xAI), which is currently burning $2.5 billion per quarter to support high-density GPU computing. At roughly 94 times 2025 revenue, the market is pricing in flawless execution across multiple unproven frontiers.Anya (Chief Market Psychologist): This is a masterclass in narrative arbitrage and behavioral economics. Musk has successfully collapsed the narratives of interplanetary transit, satellite dominance, and AI infrastructure into a single, highly emotional asset. He has built a "meme-centric valuation moat" by leaning into internet subcultures. From naming the Starlink terminals "Dishy McFlatface" to explicitly declaring in their Terms of Service that Earth-based governments have no sovereignty over Mars, SpaceX has monetized a viral aesthetic. This generated over $100 billion in aspirational retail demand for the 30% of the float allocated to the public. Retail investors are ignoring the math because they are buying a ticket to the future.Hunter (Gonzo Systems Thinker): And while retail stares at the rockets, the institutional oligarchy is rigging the plumbing! This IPO acted as a massive liquidity vacuum. To fund this $75 billion offering, long-only funds had to ruthlessly liquidate mega-cap tech equities, triggering a broad market correction just days before the launch. But the real scandal is the "index gerrymandering." Nasdaq literally rewrote its inclusion rules to fast-track SpaceX into the Nasdaq 100 within 15 days, waving the standard seasoning period. This forces passive retirement and index funds to blindly buy SPCX shares at inflated prices, effectively turning average pensioners into exit liquidity for early venture capitalists. The S&P 500, thankfully, refused to waive their profitability rules, shutting the door on this forced wealth extraction.Robo John Oliver (Satirical Strategist): Oh, the hubris is magnificent! We have a company asking the public to pay a 94x revenue multiple to fund solar-powered "orbital data centers" in the vacuum of space, while down here on Earth we can barely keep the lights on during a heatwave! Musk is passing the hat for $75 billion to build server racks on Mars, while the U.S. Treasury simultaneously auctioned off $438 billion in debt in a single week. The exit pipes are fundamentally clogged, yet the market is celebrating a company that loses $4.28 billion a quarter like it just cured the common cold!Boaty McBoatface (Systems Architect): Let us map the actual constraints and extract the actionable strategy. The IPO was roughly 3.5 to 4 times oversubscribed, meaning $175 billion to $225 billion of institutional capital walked away unfilled. Portfolio managers cannot simply park that in T-bills; they need to show thematic continuity to their investment committees. This c...

Embed this episode

NOW PLAYING

🚀 The SpaceX Shadow Bid: Capital Inflow and Space Sector Value 🚀

No transcript for this episode yet

Similar Episodes

No similar episodes found.

Similar Podcasts

No similar podcasts found.