EPISODE · Sep 24, 2025 · 13 MIN

Why You Shouldn’t Judge by PnL Alone

from Data Science Tech Brief By HackerNoon · host HackerNoon

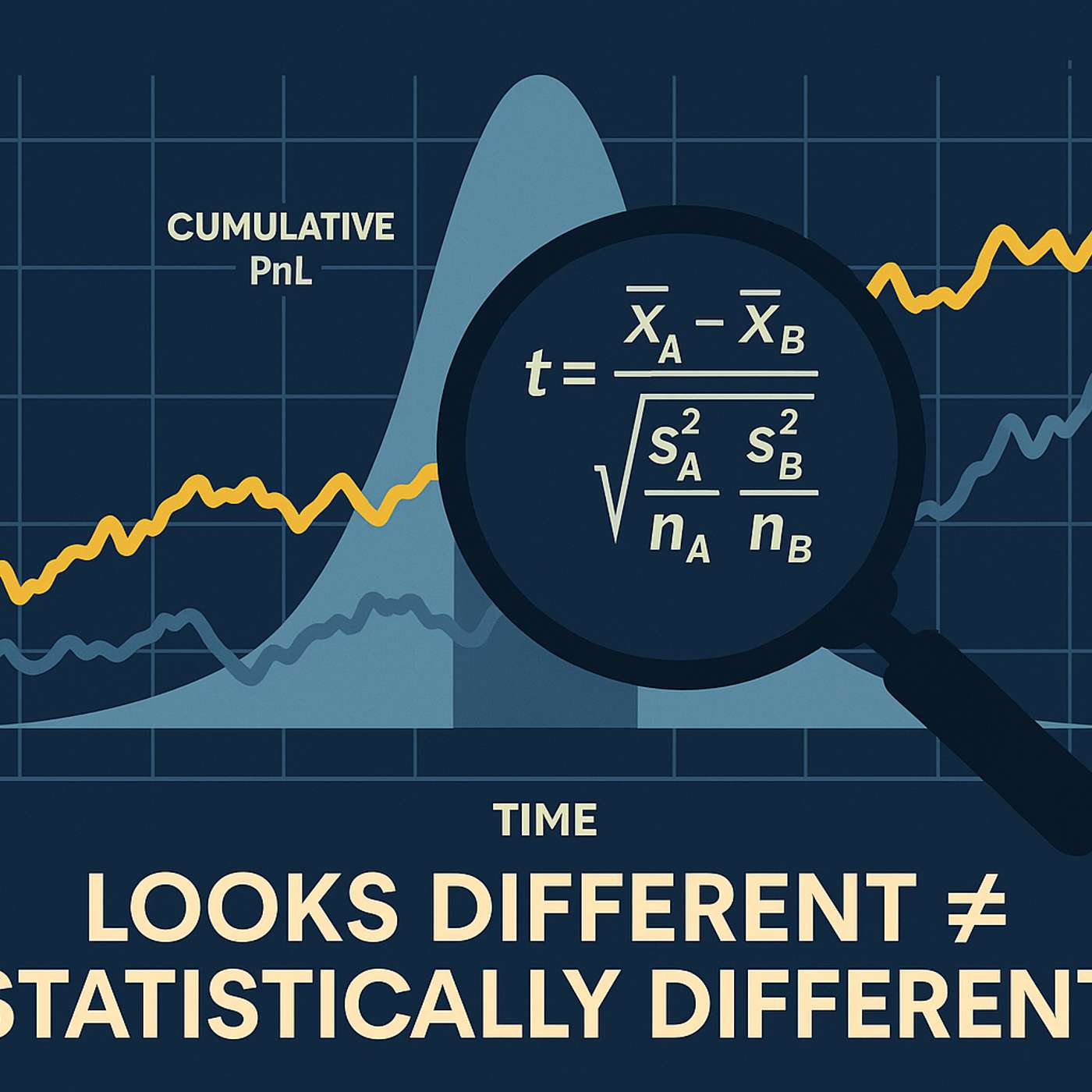

This story was originally published on HackerNoon at: https://hackernoon.com/why-you-shouldnt-judge-by-pnl-alone. PnL can lie. This hands-on guide shows traders how hypothesis testing separate luck from edge, with a Python example and tips on how not to fool yourself. Check more stories related to data-science at: https://hackernoon.com/c/data-science. You can also check exclusive content about #quantitative-research, #trading, #algorithmic-trading, #pnl, #udge-pnl, #profit-and-loss, #judge-profit-and-loss, #hackernoon-top-story, and more. This story was written by: @ruslan4ezzz. Learn more about this writer by checking @ruslan4ezzz's about page, and for more stories, please visit hackernoon.com. I’ve spent years building and evaluating systematic strategies across highly adversarial markets. When you iterate on a trading system, PnL is the goal but a terrible day-to-day signal. It’s too noisy, too path-dependent, and too easy to cherry-pick. A simple framework—form a hypothesis, measure a test statistic, translate it into a probability under a “no-effect” world (the p-value)—helps you avoid false wins, iterate faster, and ship changes that actually stick. Below I’ll show a concrete example where two strategies look very different in cumulative PnL charts, yet standard tests say there’s no meaningful difference in their average per-trade outcome. I’ll also demystify the t-test in plain language: difference of means, scaled by uncertainty.

What this episode covers

This story was originally published on HackerNoon at: https://hackernoon.com/why-you-shouldnt-judge-by-pnl-alone. PnL can lie. This hands-on guide shows traders how hypothesis testing separate luck from edge, with a Python example and tips on how not to fool yourself. Check more stories related to data-science at: https://hackernoon.com/c/data-science. You can also check exclusive content about #quantitative-research, #trading, #algorithmic-trading, #pnl, #udge-pnl, #profit-and-loss, #judge-profit-and-loss, #hackernoon-top-story, and more. This story was written by: @ruslan4ezzz. Learn more about this writer by checking @ruslan4ezzz's about page, and for more stories, please visit hackernoon.com. I’ve spent years building and evaluating systematic strategies across highly adversarial markets. When you iterate on a trading system, PnL is the goal but a terrible day-to-day signal. It’s too noisy, too path-dependent, and too easy to cherry-pick. A simple framework—form a hypothesis, measure a test statistic, translate it into a probability under a “no-effect” world (the p-value)—helps you avoid false wins, iterate faster, and ship changes that actually stick. Below I’ll show a concrete example where two strategies look very different in cumulative PnL charts, yet standard tests say there’s no meaningful difference in their average per-trade outcome. I’ll also demystify the t-test in plain language: difference of means, scaled by uncertainty.

NOW PLAYING

Why You Shouldn’t Judge by PnL Alone

No transcript for this episode yet

Similar Episodes

Mar 26, 2026 ·1m

Jan 2, 2026 ·47m

Dec 21, 2025 ·46m